Article from Canadian Mortgage Trends

In September, nearly all of Canada’s Big-6 banks have increased their shorter-term fixed mortgage rates.

The rate hikes have largely been limited to 1-, 2- and 3-year fixed mortgage products, including both special offer and posted mortgage rates. The hikes were seen at TD, Scotiabank, RBC, BMO and National Bank of Canada, and range from 10 to 55 basis points.

But the big banks haven’t been the only lenders raising rates on those terms.

According to data from MortgageLogic.news, the average nationally available deep-discount rates for uninsured 1- and 2-year fixed rates have jumped by 27 bps and 22 bps, respectively, since the beginning of the month. In comparison, average uninsured 5-year fixed rates rose 5 bps over the same period.

Ryan Sims, a mortgage broker with TMG The Mortgage Group and former investment banker, said yield curve inversion is the main culprit.

“It is very true that shorter-term fixed rates have moved a lot more,” he told CMT. “Currently, we are seeing the 1- and 2-year notes yield far more than a 5-year note.

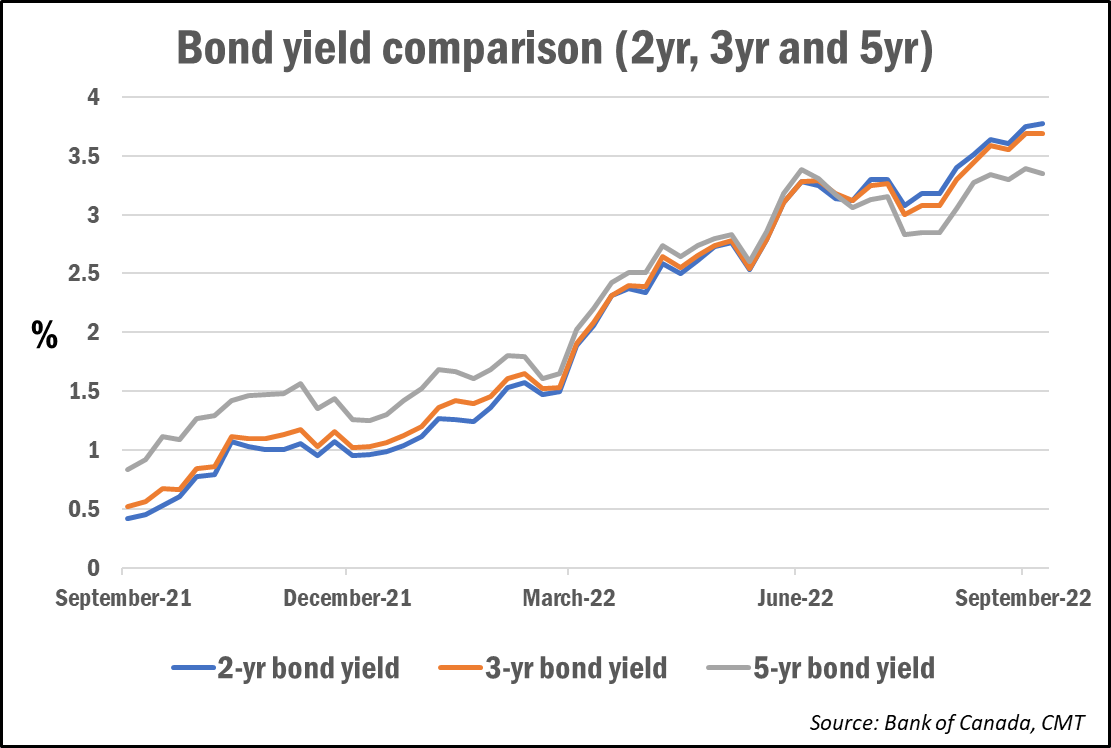

- Jargon Buster: What is yield curve inversion? Yield curve inversion happens when shorter-term interest rates rise above longer-term rates in the bond market. This indicates more investor money is moving into longer-term bonds, and typically signals growing pessimism about near-term economic prospects.

As the graph below demonstrates, both 2- and 3-year bond yields have now risen above 5-year bond yields:

So, why is this happening?

As mentioned above, there’s been growing volatility in near-term economic sentiment among investors.

“Recent economic data has been coming in consistently on the negative side,” Sims noted, pointing to declining GDP in July and August, rising unemployment since June, and net job losses in August that “rivalled monthly data not seen since the Great Financial Crisis of 2008.”

“While yield curve inversion is a topic of much debate, the length of time the curve has been inverted and the sheer amount that the curve is inverted signals to me that a recession is coming, and that it will not be routine,” he said.

“The BOC has signalled that fighting inflation is their only goal, but I think they have to be wary of the medicine being stronger than the diagnosis,” he added. “Inflation is a problem, but if we raise too far, too fast, then we risk the solution being greater than the problem we were trying to solve.”

What can mortgage shoppers do?

Given the sharp and rapid rise of mortgage rates over the course of the year, many mortgage borrowers—both new borrowers and those renewing—have gravitated towards shorter-term rates, which are generally priced lower than most 5-year terms.

Data from the bank of Canada shows the volume of mortgages advanced for new and existing lending from chartered banks has shifted towards terms under five years.

Between March and July (the latest data available), funds advanced for 1- to 3-year fixed terms rose by roughly 40% (for both insured and uninsured mortgages), while volumes for insured and uninsured 5-year fixed terms were down 13% and 5%, respectively.

Sims added that another reason for the recent rate increases, aside from yield curve inversion, could be that the banks have “figured out where consumer sentiment is.”

What strategy does that leave for today’s borrowers?

Rate expert Rob McLister, editor of MortgageLogic.news, says the best value is still generally found in the shorter terms.

“Everyone’s needs are different, but the sweet spot for most well-qualified borrowers is any 1- to 3-year fixed term near/below 4.50%,” he told CMT. While his rate simulations are run using the OIS-implied rate path, “that doesn’t mean these are guaranteed to be the best-performing terms.”

Another hedge for borrowers can be to spread their mortgage between both a fixed and variable rate with a hybrid mortgage.

“Term selection is first about risk management,” he says. “If a 20% jump in your payment would break your family budget, mitigate risk with a hybrid or (at least) medium-term fixed mortgage. The more qualified and liquid you are, the more you can gamble on: (A) a shorter term, or (B) added variable exposure in a hybrid.”

The latest rate forecasts

The following are the latest interest rate and bond yield forecasts from the Big 6 banks, with any changes from their previous forecasts in parenthesis.

| Target Rate: Year-end ’22 |

Target Rate: Year-end ’23 |

Target Rate: Year-end ’24 |

5-Year BoC Bond Yield: Year-end ’22 |

5-Year BoC Bond Yield: Year-end ’23 |

|

| BMO | 3.75% (+25bps) | 3.75% (+25bps) | NA | 3.30% (10bps) | 3.05% (+5bps) |

| CIBC | 3.75% (+50bps) | 3.75% (+50bps) | NA | NA | NA |

| NBC | 3.75% (+50bps) | 3.00% (-25bps) | NA | 3.25% (+5bps) | 3.05% (+5bps) |

| RBC | 4.00% (50bps) | 3.75% (+50bps) | NA | 3.00% (+20bps) | 2.50% (+10bps) |

| Scotia | 3.75% (+25bps) | 3.75% (+25bps) | NA | 3.45% (+15bps) | 3.15% (+15bps) |

| TD | 4.00% (+50bps) | 4.00% (+75bps) | NA | 3.45% (+60bps) | 2.55% (+25bps) |

Recent Comments